You can fall in love with a downtown Sarasota view in seconds, but the building’s budget determines what you will pay and the risks you take. If you are eyeing the luxury towers in 34236, understanding how to read a condominium budget is essential. You want clarity on monthly fees, future projects, insurance exposure, and the likelihood of special assessments. This guide walks you through what to look for, what to ask, and how to compare buildings with confidence. Let’s dive in.

What a condo budget really shows

A condominium budget has two main parts: the operating budget and the reserves. Operating expenses cover the day-to-day costs you fund through monthly assessments. Reserves are savings for predictable big-ticket replacements.

You will also see non-assessment income and sometimes debt service. Income from guest suites, marina slips, event rentals, or interest helps lower what owners pay. If the association borrowed for a past project, loan payments may appear as debt service and are typically included in assessments.

Operating vs. reserves

- Operating budget: utilities for common areas, maintenance contracts, management, staffing, insurance, and routine repairs. These recur every year.

- Reserves: savings for major components with a known useful life, such as roof, elevators, chillers, façade repairs, balconies, windows and doors, parking structures, and in waterfront buildings, seawalls and docks.

- Why it matters: operating costs affect your monthly fees now, while reserves tell you how well the building is preparing for future work. Underfunded reserves often lead to special assessments.

Income and debt service

- Non-assessment income: guest suite fees, amenity rentals, marina slip fees, and interest income can offset expenses.

- Debt service: if the association financed a project, you may see principal and interest listed. This can be a sign of past improvements, but it increases monthly costs until paid off.

Key line items to review

Look beyond the total and scan the line items. Focus on the big drivers and what they imply for risk and future costs.

- Insurance, master policy: check coverage scope, whether wind and flood are included, deductible amounts, carrier stability, and premium trends. In Florida, insurance often dominates budgets, and high hurricane deductibles can mean large owner assessments after a major storm.

- Utilities: common area electricity, water, sewer, gas, and sometimes central plant costs. In some towers, a central HVAC plant serves units, which concentrates capital needs in reserves.

- Maintenance and repairs: elevator contracts, HVAC and chiller service, pool and spa, landscaping, pest control. Long contracts with auto-renewals can lock in rising costs.

- Management fees and payroll: doorman, concierge, valet, security, cleaning, and on-site management. Luxury staffing raises quality of life and expense.

- Legal and accounting: spikes can signal litigation or large projects.

- Amenity operations: fitness centers, restaurants, spa facilities, marina. Confirm whether fees offset costs or if amenities are net cost centers.

- Reserve contribution: compare the annual contribution to the reserve study’s recommendation to spot shortfalls.

- Capital projects and debt service: identify planned work and how it will be funded.

Reserve studies and funding health

A reserve study estimates the remaining life and replacement cost of major components, then recommends annual contributions.

What to request

- Date and type of study: full study or update, and the assumptions used for cost inflation and useful lives.

- Current reserve balance and trends: is the balance growing, steady, or declining year over year?

- Funding ratio: the percentage of reserves on hand relative to estimated needs. There is no universal “right” number, but the ratio and trend tell you a lot.

- Near-term projects: ask what replacements are expected in the next 5 to 10 years and how they will be funded.

How to interpret the numbers

- Compare the budget’s annual reserve contribution to the study’s recommended contribution. A large gap is a warning.

- Review the history of special assessments. Repeated “emergency” assessments or transfers from reserves to operating can indicate chronic underfunding.

- Look for clear plans to fund known projects. If major work is listed without a funding source, expect an assessment or borrowing.

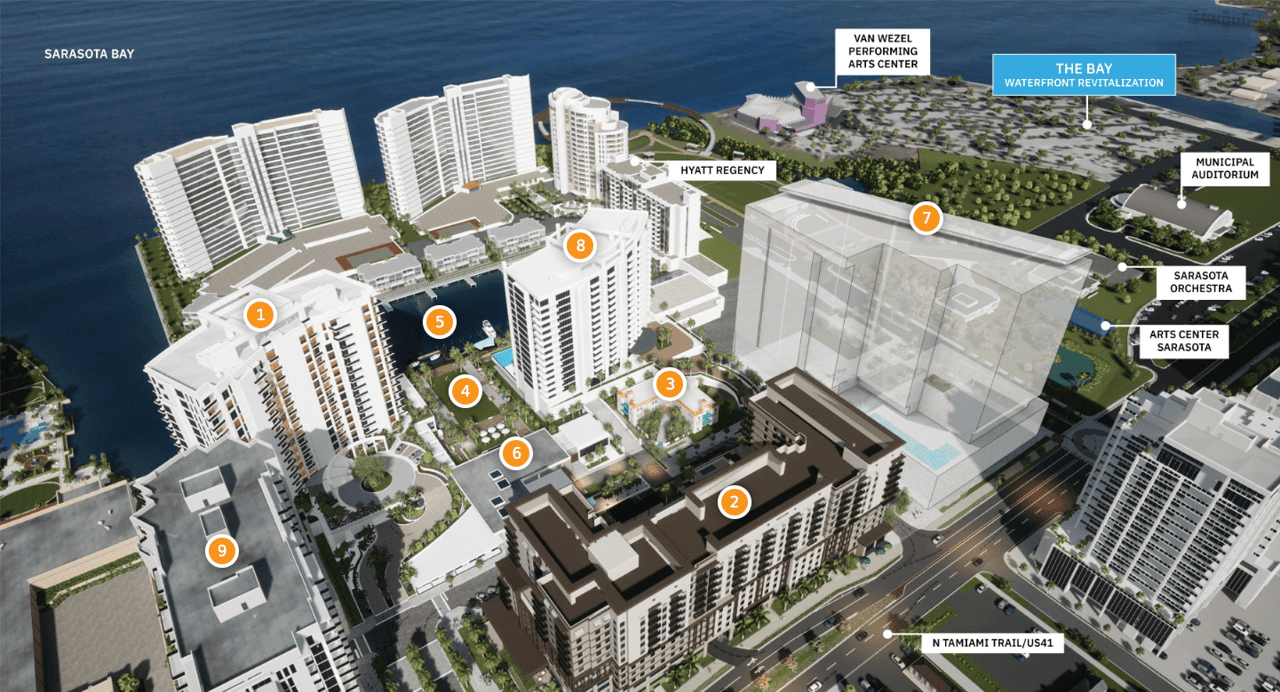

Sarasota high-rise realities

- Coastal exposure: salt air and humidity accelerate concrete spall repairs, balcony and railing replacements, and window and sealant maintenance.

- Central plants and elevators: chillers and elevator modernizations are big capital items that should appear in the reserve plan.

- Waterfront infrastructure: seawalls, docks, and marinas require specialized maintenance and can be costly.

Insurance in Florida: what to verify

Insurance is a major budget driver and a key risk factor in coastal Florida.

- Master policy scope: confirm building property, liability, and fidelity coverage. Many policies exclude flood for common elements, so verify if separate flood coverage exists.

- Wind and hurricane deductibles: often expressed as a percent of insured value. High deductibles can translate to substantial special assessments after a storm.

- Premium trend and carriers: review renewal history and any recent carrier changes or non-renewals.

- Claims history: frequent or severe claims, especially water intrusion or wind, can raise costs.

- Flood zones: confirm the building’s flood designation and whether lenders will require separate flood policies for your unit.

Amenity trade-offs in luxury towers

Amenities shape your lifestyle and your budget. Decide what you will truly use and how costs are shared.

- 24/7 concierge and valet: elevate service but create high, predictable personnel costs.

- Fitness, pool, and spa: ongoing maintenance for HVAC, pumps, tile, and finishes can be significant in larger facilities.

- On-site dining or catering: may generate revenue through a third-party operator, but can add variable costs and regulatory complexity.

- Private marina or docks: specialized insurance, piling and hardware maintenance, dredging, and seawall work. Fees may or may not offset costs.

- Central HVAC plants: less in-unit equipment to maintain, but major shared capital when overhaul is due.

- Parking garages and lifts: require structural upkeep and specialized service contracts.

Evaluate usage, any revenue offset, and how costs are allocated. Some associations assess by unit size or charge separate fees for certain amenities.

Red flags to watch for

Spot issues early by scanning budgets, financials, and minutes.

- Very low or declining reserve balances versus recommendations.

- Recent or recurring large special assessments.

- High or rising delinquency rates on owner dues.

- Large transfers from reserves to cover basic operating costs.

- Sudden spikes in insurance premiums or insurer non-renewal.

- Frequent spikes in legal or repair line items.

- Gaps or irregularities in minutes or financial reporting.

- Active litigation without clear funding plans.

- Opaque communication or resistance to reasonable document requests.

- Marina and seawall assets with unclear maintenance records or missing permits.

Quick math to compare buildings

To estimate monthly assessments, use a simple formula:

(Annual operating expenses + annual reserve funding + annual debt service − non-assessment income) ÷ number of units = annual assessment per unit. Divide by 12 for monthly.

Tips for apples-to-apples comparisons:

- Compare total monthly assessment, not just select line items.

- Normalize by square footage when unit sizes vary to spot outliers.

- Adjust for age and near-term capital projects. A lower fee today can mask underfunded reserves and future assessments.

- Trend check: are assessments rising faster than typical inflation or local income growth over several years?

What to collect and what to ask

Getting the right documents is half the battle. Insist on actual PDFs, not summaries.

Priority documents

- Current year budget and prior 2 to 3 years of budgets.

- Most recent reserve study and updates.

- Last 3 years of financial statements and current year-to-date financials.

- Current reserve account statements.

- Board meeting minutes for the last 12 months, or 24 months for higher-risk buildings.

- Insurance declarations for the master policy and any separate wind or flood coverage.

- List of pending or threatened litigation and legal opinions.

- Major vendor and service contracts, including management, security, elevator, HVAC, and landscaping.

- Schedule of regular and special assessments, plus recent special-assessment history.

- Records of recent capital projects with permits and warranties.

- Owner delinquency report and percentage outstanding.

- Governing documents for rules on rentals, pets, and assessment collection.

Direct questions for managers, boards, and sellers

- What is the current reserve balance and how does it compare to the study’s recommended balance?

- When was the last full reserve study completed and when is the next one scheduled?

- What capital projects are planned in the next 1 to 5 years and how will they be funded?

- What special assessments have occurred in the last 5 years and why?

- What is the association’s delinquency rate and how are collections handled?

- Are there pending lawsuits that could affect assessments? What is the status?

- What exactly does the master insurance cover, and what are the wind and flood deductibles?

- Are management fees, insurance, utilities, or other expenses forecasted to increase?

- Are any building systems on a deferred maintenance schedule?

- Are there policies regarding reserve funding or caps on assessment increases?

- For waterfront buildings: what is the condition and permit status of seawalls, docks, and marina facilities?

Your timeline

- Before contract: review budgets, reserve study, financials, insurance declarations, and recent minutes.

- During inspection and escrow: request an updated estoppel or financial statement listing current assessments, pending special assessments, and any delinquencies or liens.

- If concerns arise: consider a condominium attorney for disclosure questions and a reserve or engineering consultant if major work is suspected.

Sarasota specifics for 34236 buyers

Downtown Sarasota combines older high-rises with newer luxury towers. Age, construction type, and waterfront exposure drive both operating costs and reserve needs.

- Salt air and humidity increase building envelope maintenance, balcony and railing work, and window and sealant cycles.

- Central chiller plants and elevator modernizations are common capital items in taller buildings.

- For waterfront properties, seawalls, docks, and marinas add specialized maintenance and permitting considerations.

- Pull permit histories for major projects such as concrete restoration, façade work, and elevator upgrades. Verify contractor warranties where available.

- Confirm flood zone designation and whether flood insurance is in place for common elements. Lenders may require separate flood coverage for your unit.

Next steps

Approach each building with a checklist and a clear plan.

- Gather and review the core documents listed above.

- Compare total monthly assessments and reserve funding trends across buildings you are considering.

- Map out near-term projects and likely funding paths so you are not surprised by a future assessment.

- Align amenities and service levels with your actual use and expense tolerance.

- For waterfront towers, confirm the condition and permitting of seawalls and marina elements.

When you want a second set of eyes on a budget or reserve study, or you need introductions to local insurance and engineering pros, reach out to the team that lives and works downtown. Tell us your story, and let us help you choose the right tower with confidence. Connect with the experts at Schafer Real Estate.

FAQs

What is a condo reserve study in Sarasota’s luxury towers?

- It is an assessment of major building components and their replacement timelines and costs, used to set annual reserve contributions and plan for projects like façades, chillers, elevators, and seawalls.

How can I tell if reserves are healthy before I buy?

- Compare the current reserve balance and annual contribution to the reserve study’s recommendations, review the funding ratio and trend, and look for a clear plan for projects in the next 5 to 10 years.

How do hurricane deductibles affect owners in 34236?

- Many master policies use high wind deductibles as a percentage of insured value, which can lead to large special assessments on owners after a major storm event.

Are flood policies usually included in condo fees?

- Flood is often excluded from the master policy, so confirm if the association carries separate flood coverage for common elements and whether your lender will require an individual flood policy.

What amenities tend to raise monthly fees the most?

- Full-time concierge and valet, extensive fitness and spa facilities, central HVAC plants, parking structures, and marinas typically add significant operating and long-term capital costs.

What documents should I request before making an offer in downtown Sarasota?

- Ask for the current and recent budgets, reserve study, 3 years of financials, insurance declarations, recent board minutes, vendor contracts, litigation list, assessment history, reserve statements, and governing documents.